Opportunities for the SEFE Group

The SEFE Group sees growth opportunities in a dynamic market driven by the changes in demand due to the energy transition, electrification and digitalisation. The Group is also strategically well-positioned to meet the increased need for secure supply sources and stable infrastructure resulting from geopolitical developments. Expected new regulations for hydrogen, carbon capture and storage, updated requirements regarding the security of supply and national market reforms will result in further investment opportunities for the Group.

The balanced sales and origination strategy as well as the Group’s expertise in the global LNG and European natural gas and power markets form the basis for long-term growth and enable a dynamic response to short-term market opportunities. This makes it possible to build long-term customer relationships and exploit origination advantages. Established partnerships and a diversified customer base enable the Group to further expand its pipeline gas and LNG portfolios through medium- and long-term transactions, thereby a contributing to the security of supply in Europe. In the short term, the SEFE Group can exploit the flexibility of its portfolio to generate margins and create added value for the shareholder and customers.

In the medium term, the SEFE Group has opportunities to drive growth and strengthen its market position. The further expansion of digital trading with increasing use of artificial intelligence and the implementation of algorithmic strategies will provide the Group with the opportunity to optimise its trading activities.

In the power markets, the focus is on flexibility, balancing group management and risk services. The SEFE Group can develop options to diversify its revenue by optimising its digitalisation, expanding its portfolio of embedded power purchase agreements, boosting its trading in green certificates and entering new commodity markets. This includes metals trading, which enables access to important raw materials and strategic supply chains that are a prerequisite for technologies related to the energy transition.

The SEFE Group’s long-term strategy is in line with the goals of ensuring the security and affordability of the energy supply and supporting decarbonisation. The regulated infrastructure activities offer long-term opportunities regarding the future hydrogen network. Key projects in this regard include “Flow – making hydrogen happen”, which envisages the development of hydrogen transport capacity in Germany and the Netherlands, and AquaDuctus, which aims to facilitate offshore hydrogen production and transport from wind farms in the North Sea. This enables predictable income and positions the Group as a driver of new technologies and decarbonisation. Given the dynamic development in the technological, economic and regulatory framework, the Group is examining various ways to achieve these goals. This also includes developing partnerships and internal expertise in carbon-related value chains.

The SEFE Group’s diverse capabilities also enable the effective management of risks and the exploitation of opportunities in volatile markets. The Group relies on advances in trading, portfolio management and product innovation to ensure long-term growth and competitiveness.

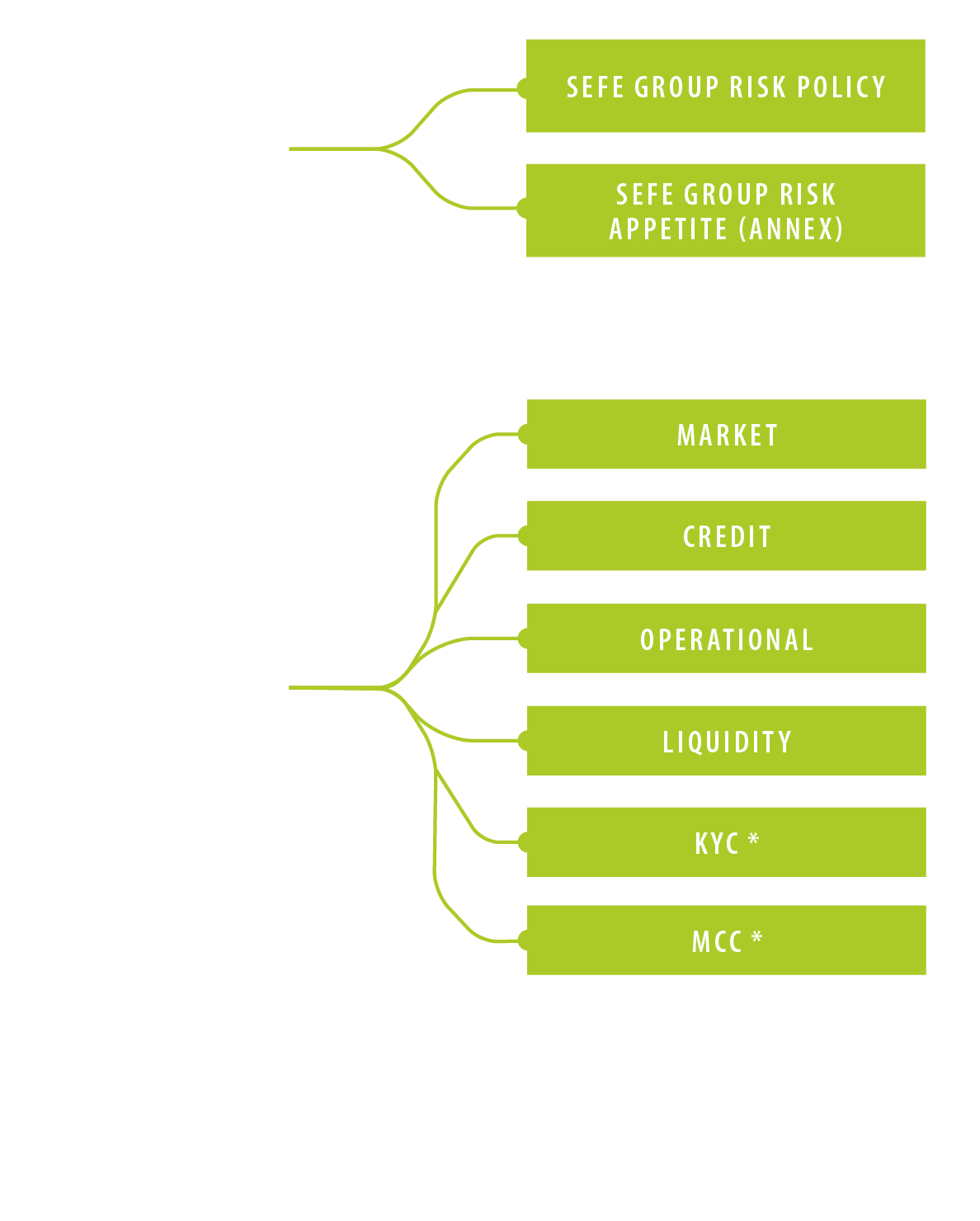

Risk management system of the SEFE Group

The SEFE Group’s risk management, which is an integral component of the Group’s business processes, adapts continuously to evolving market conditions, regulatory changes, strategic priorities and overarching business objectives. It is based on a consistent, Group-wide system for identifying, assessing and managing financial and non-financial risks. This system, which is supplemented when needed by appropriate mitigation measures, ensures uniform and effective monitoring of operating and financial activities.

The risk management system, which takes into account organisation-wide unbundling requirements, is a key component for achieving the Group’s objectives. The Group expanded the risk management framework in the 2025 reporting year to include ESG aspects. This expansion included implementing processes for the systematic identification and assessment of environmental risks, aligning risk considerations more closely with financial planning periods, and conducting scenario analyses to quantify significant transition and physical risks.

Risk management

The SEFE Group’s risk management system, which is documented in internal guidelines and methods, ensures a structured approach to risk management. The overarching risk framework is defined by the risk policy and risk appetite established by the SEEHG Supervisory Board, while the detailed implementation is governed by subordinate guidelines and supporting documents issued by the Management Council – a body comprised of key members of management – and by the central Group Risk Management function.

| IMPACT CLASSES |

| Level |

Likelihood

in % |

Impact

in € million |

| Minimal |

0–25 |

0–5 |

| Low |

25–60 |

5–50 |

| Medium |

60–80 |

50–250 |

| High |

80–100 |

> 250 |

The SEFE Group’s risk appetite comprises quantitative limits for financial risks and qualitative statements on risk tolerance for non-financial risks. The system is therefore designed to ensure the continuous and consistent implementation of controlled risk management across the entire Group. The Group has established two risk committees to ensure an effective governance structure. These committees, one appointed by the Supervisory Board and one by the Management Council, monitor compliance with the defined risk limits, provide advice on risk-related issues, and support the ongoing enhancement of the system.

| RISK ASSESSMENT |

| Risks |

Likelihood |

Impact |

| Market and portfolio risks |

Low |

High |

| Liquidity risks |

Minimal |

High |

| Credit risks |

Minimal |

Medium |

| IT and resilience risks |

Medium |

High |

| Strategic risks |

Low |

High |

| Political and regulatory risks |

Low |

High |

| Operational risks |

Medium |

Medium |

| Legal risks |

Medium |

Low |

| Compliance risks |

Medium |

Low |

The operating and supporting units act as risk owners and manage risks within their operating activities. The SEFE Risk Management function acts as a second line of defence and provides advisory services, independent control functions, reporting and monitoring, thereby ensuring the consistent application of risk policies.

Risk identification and evaluation

The assessment of potential impacts and likelihoods forms the risk management framework that enables the Group to set priorities and manage risks effectively. The SEFE Group distinguishes between financial and non-financial risks to take into account the direct impact of certain risks on the Group’s financial position.

The probability of occurrence is determined based on historical data or qualitative assessments and ranges from minimal to high. Potential risks impacting the financial key performance indicators, ESG-related focal points and business operations are classified on a scale from minimal to high.

The risk exposures for the SEFE Group are classified into nine categories. The classification of each risk category is determined by a qualitative assessment based on the average assessment of all individual risks within that category.

The observation horizon depends on the type of risk and is usually one year. Medium- to long-term periods are included in the assessment in individual cases.

Financial risks

The SEFE Group’s business activities result in market and portfolio risks, as well as credit and liquidity risks. The Group uses numerical models to quantify and control these financial risks. These risks are managed in accordance with the parameters defined in the Group-wide risk appetite.

Market and portfolio risks result from the main risk drivers in the commodity portfolio, such as the development of commodity and derivatives prices, exchange rates, interest rates and price volatility in trading and sales, supplemented by the dynamics of the emerging markets for low-emission energy sources. The long-term LNG contract portfolio represents the dominant risk exposure in this regard.

In the Infrastructure business area, market prices are influenced primarily by summer/winter price spreads. Current challenges include persistently low volatility in commodity markets, decreasing or even inverted seasonal price differentials, and the need for continuous strategic adaptation to the pace of the energy transition.

Market risk is measured using the metric market value at risk (MVaR), which is determined through Monte Carlo simulation and supplemented by stress tests, sensitivity analyses, correlation/diversification models, risk limits and scenario analyses for long-term risks. Market risk is accepted within defined limits, with risk management supported by a Group-wide EBITDA monitoring framework and a stringent cost management programme.

The assessment of the SEFE Group’s market risks remained unchanged compared with the previous year.

Liquidity risks arise primarily from potential negative deviations from planned cash flows resulting from the risks of the SEFE Group. Liquidity is monitored through the ongoing comparison of financial obligations with the available cash and committed credit lines.

To manage these risks, the Group identifies the maturity-dependent obligations that must be covered by available liquidity, including committed credit lines. The Group’s financing is secured through available credit lines, even under challenging market conditions. The assessment of the SEFE Group’s liquidity risk remained unchanged compared to the previous year.

Credit risks result from the possibility that counterparties do not fulfil their contractual obligations, which can negatively impact the SEFE Group’s financial performance. These risks arise mainly from the Group’s sales and trading activities, where credit risks are continuously monitored and managed.

In 2025, the SEFE Group’s overall exposure to credit risk decreased compared to the previous year. This improvement resulted from several factors, including a decrease in the overall exposure due to falling commodity prices and lower market volatility, as well as upgrades in the credit ratings of insurers, which cover a large part of the retail portfolio.

The Group’s approach to credit risk management includes the assessment of counterparties’ creditworthiness, processes for monitoring credit exposures and the application of credit limits.

Non-financial risks

The SEFE Group manages non-financial risks through central controls that are based on the qualitative risk definitions of the risk appetite. Operational risks are minimised to an acceptable level, taking economic efficiency into account. Strategic risks are integrated into decision-making processes to limit their impact. The Group also proactively implements measures to minimise health, safety and environmental (HSE) risks. A zero-tolerance policy applies to regulatory violations.

The following section provides an overview of the SEFE Group’s approach to managing non-financial risks. It also describes the significant developments during the reporting period in the respective risk categories.

IT security and resilience risks occur in connection with the availability, security and adequacy of IT systems and technological resources. As privatisation progresses, there is an elevated risk of targeted attacks by state-sponsored actors. Such attacks could jeopardise business continuity and cause significant financial losses and operating disruptions.

To mitigate these risks, the SEFE Group is continuously improving the resilience of its IT infrastructure by migrating to cloud environments and implementing robust disaster recovery and high-availability solutions. Furthermore, the Group has deployed a new security programme to enhance existing security controls and minimise exposure to ransomware, insider threats and regulatory non-compliance.

Key measures include Group-wide security policies and a strengthened security and incident response framework, which incorporates intelligent monitoring and insider threat mitigation. In addition, contingency and resilience plans are regularly updated to ensure a consistent and resilient level of security across the entire Group. The assessment of the SEFE Group’s IT security and resilience risks remained unchanged compared to the previous year.

Strategic risks result from the SEFE Group’s long-term objectives, including safeguarding the security of supply through the conclusion of long-term gas supply contracts and securing regasification capacity. The interplay between the requirements of supply security, weaker gas demand in Europe and accelerated decarbonisation poses significant challenges. The benefits of long-term supply contracts, for example, could be offset by the need for decarbonisation, thereby negatively affecting trading revenue through lower prices and reduced volatility.

The long-term profitability in the Infrastructure business area is subject to uncertainties that result primarily from the currently low and sometimes inverted seasonal price spreads in the storage business, the gradual substitution of natural gas with alternative energy sources, and the significant investments necessary in connection with the planned conversion to hydrogen-ready applications. At the same time, the strategic provision of storage capacity and the gradual transformation of the infrastructure to hydrogen offer substantial value creation potential for the SEFE Group in the future.

EU-imposed restrictions in connection with the state ownership structure currently limit the Group’s strategic options.

In the Sales business area, the Group faces ongoing challenges in keeping the existing business resilient while meeting growing customer demands for digitalisation, decarbonisation, compliance with high ESG standards and adaptation to the energy transition. To mitigate risk, the SEFE Group conducts ongoing market analyses and regular contract reviews, supplemented by quarterly updates to the long-term market and risk framework. The assessment of the SEFE Group’s strategic risks remained unchanged compared to the previous year.

Political and regulatory risks encompass both geopolitical risks and risks arising from regulatory changes, which are assessed in a Group-wide risk matrix. Geopolitical risks are a significant driver within this category, as their importance for strategic decision-making in the context of global political dynamics continues to grow. This includes the risk of further military escalation in the Middle East, which could lead to significant disruptions in global supply chains and result in rising energy prices, additional inflationary pressure, tightened sanctions, and a deterioration of the economic growth outlook.

One political risk that was particularly relevant during the reporting year was the EU’s implementation of a complete import ban on LNG from Russia, which will lead to a reduction in future earnings. To prepare for potential sanctions-related impacts, the Group performs scenario analyses, conducts intensive dialogue with stakeholders, and maintains a diversified origination portfolio. The Group considers the uncertainties arising from global tariffs policy to represent only indirect exposures that are immaterial to the Group.

The comparatively low risk of regulatory changes results from existing and planned regulations that necessitate additional infrastructure investments, increase the costs of trading strategies, and may challenge the resilience of IT systems.

While the SEFE Group actively monitors global political and regulatory developments, it also takes measures to mitigate potential impacts by working with policymakers and industry associations and by diversifying its supply portfolio. The assessment of the SEFE Group’s political and regulatory risks remained unchanged compared to the previous year.

Operational risks encompass financial and non-financial risks that may result from inadequate or faulty processes, human error, system failures and external events. The increase compared to the previous year is mainly due to the transfer of certain risks from other risk categories. As a result of this reclassification, operational risk is reported separately in the 2025 financial year; it was included under Other Risks in the previous year.

The increase in operational risk is also attributable to the Group’s ongoing organisational and IT transformation. To manage operational risks, the SEFE Group is strengthening the governance in its IT portfolio, aligning initiatives more consistently with strategic priorities, and developing contingency plans with corresponding reserve capacity. The implementation of these plans is scheduled to be finalised in 2026.

The expansion of the LNG portfolio also entails additional risks related to potential incidents on chartered LNG vessels. The Group addresses these risks by implementing specific contingency and crisis response plans and establishing appropriate insurance coverage to limit the impact on the Group’s operations and financial stability.

Legal risks within the SEFE Group are assessed in the reporting year as having an increased likelihood of occurrence and a slightly reduced impact. The increase in the likelihood of risk occurrence is attributable primarily to the risk that a change of control could have on existing contracts. The potential loss amount decreased, however, because several arbitration proceedings were concluded during the year.

The Group recognises provisions if legal proceedings exist and it is likely that financial commitments will materialise as a result.

Compliance risks arise from complex and rapidly changing regulatory requirements, fragmented and regionally different compliance standards and mounting regulatory oversight.

The risk increased during the reporting year and, due to its greater relevance, is reported for the first time as a separate risk category. This increase results from related aspects of the risk management system that can be improved, including compliance processes, control mechanisms and governance structures, as well as from stricter regulatory enforcement measures, particularly in connection with French energy efficiency certificates. These measures had a financial impact in 2025 and led to an adjustment in the risk assessment, thereby increasing the likelihood of occurrence compared to the previous year.

The risk stems fundamentally from the high complexity and dynamism of regulatory requirements, which are further amplified by differing national and regional requirements and mounting supervisory activities.

To mitigate this risk, the SEFE Group has established a second line of defence within its Compliance function, which is responsible for Group-wide regulatory oversight. Active monitoring and enhanced governance measures increase the transparency of regulatory risks and sustainably strengthen the Group’s resilience to compliance violations.

Other risks encompass additional, continuously monitored risk areas that are typically encountered in the energy sector. These include financial, personnel and transformation risks. All risks included in this category are classified as low.

The Group manages these risks in the same way as other non-financial risks and ensures that even minor risks are adequately considered and addressed promptly. It does not, however, apply special features that surpass the industry standard.

Potential risks related to the Group’s infrastructure, as well as HSE and ESG risks, are distributed across the risk categories mentioned above.

Overall assessment of opportunities and risks

The SEFE Group’s current risk and opportunity profile reflects the dynamic transformation of the energy sector, which is driven primarily by the global transition to a low-carbon economy and ongoing technological innovation. Strategic risks arise in particular from the challenge of reconciling long-term gas supply contracts with declining European gas demand and accelerated decarbonisation. In the Management’s assessment, however, there are no existential risks at the date when this annual report was prepared.

Despite these challenges, strategic opportunities are also emerging for the SEFE Group. Long-term LNG contracts and alternative pipeline sources strengthen the security of supply and resilience, while the Group’s transport infrastructure ensures stable margins and operating flexibility. Targeted investments in decarbonised energy solutions create further growth opportunities. Factors that enhance the Group’s efficiency and competitiveness include the use of digital technologies and the increased deployment of artificial intelligence, algorithmic optimisation and scalable processes. Furthermore, the planned development of trading platforms for strategically important metals creates additional value creation potential in an increasingly electrified economy.

Overall, the SEFE Group considers itself well positioned to help shape the decarbonisation of the economy through its integrated business model, forward-looking risk management and targeted investments in low-carbon technologies.